In the world of personal finance, “Debt” is usually treated as a four-letter word.

We are taught from a young age that debt is dangerous. We are told to cut up our credit cards, pay for everything in cash, and live completely debt-free. For 90% of the population, this is excellent advice. If you cannot control your spending, debt is a chainsaw that will cut your financial legs off.

But if you look at the financial statements of the ultra-wealthy—real estate tycoons, business owners, and Fortune 500 companies—you will notice something strange: They all have debt. Lots of it.

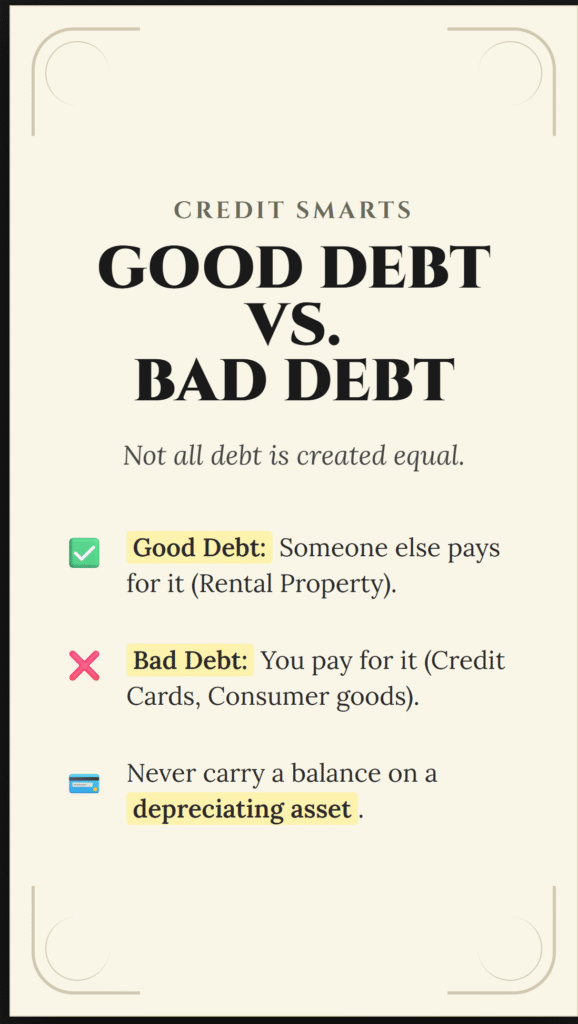

Why? Are they reckless? No. They understand a secret that most people don’t: Not all debt is created equal.

There is a massive difference between debt that makes you poor and debt that makes you rich. One is a master that enslaves you; the other is a tool that serves you.

To build true wealth, you must stop fearing debt and start understanding it. You need to learn the art of Leverage.

This guide will break down the mathematics, the psychology, and the strategy behind Good Debt vs. Bad Debt.

Part 1: The Concept of Leverage

Before we categorize debt, we must define the mechanism behind it. In finance, debt is referred to as “Leverage.”

Think of a physical lever. If you want to lift a 500-pound rock, you cannot do it with your bare hands. But if you use a long metal bar (a lever) and a fulcrum, you can lift that rock with very little effort. You are multiplying your strength.

Financial Leverage works the same way. It allows you to use a small amount of your own money to control a large, expensive asset.

- Without Leverage: You need $500,000 cash to buy a $500,000 building.

- With Leverage: You need $100,000 cash (down payment) and a bank loan to buy that same $500,000 building.

In both scenarios, you own the building. But in the second scenario, you have “lifted the rock” using only 20% of the effort (cash). This magnification of power is how wealth is built rapidly. However, if the lever snaps, it crushes you. This is why distinguishing between Good and Bad debt is the most important skill in finance.

Part 2: The Villain (Bad Debt)

Let’s start with the debt you must avoid at all costs. This is the “Consumer Debt” that keeps the middle class running on a hamster wheel.

The Definition

Bad Debt is money borrowed to purchase an asset that depreciates in value and generates no income.

When you take on bad debt, you are signing a contract to make yourself poorer in the future to feel good today. You are paying interest on something that will be worth less tomorrow than it is right now.

The Characteristics of Bad Debt

- High Interest Rates: Usually exceeds 10%, often reaching 20-30%.

- Non-Deductible: The government offers no tax breaks for holding this debt.

- Depreciating Asset: The underlying item loses value immediately.

- Personal Guarantee: You are personally liable for the repayment, often with your future wages.

Examples of Bad Debt

1. Credit Cards

Credit card debt is the most toxic financial substance known to man. With average interest rates hovering around 24% (as of 2024/2025), it destroys wealth mathematically.

The Math of Misery: If you have a $10,000 balance on a card with 20% APR and you only make the minimum payment:

- It will take you over 25 years to pay it off.

- You will pay roughly $15,000 in interest alone.

- That $10,000 purchase actually cost you $25,000.

2. Auto Loans (for Luxury/New Cars)

As discussed in previous articles, cars are depreciating assets. They lose 20-30% of their value in the first year. When you borrow money at 7% interest to buy an asset that drops 20% in value, you are burning the candle at both ends. You are paying the bank for the privilege of losing equity.

- The Trap: Dealerships focus on “Monthly Payments.” They will extend a loan to 84 months (7 years) to lower the payment. This keeps you in debt for nearly a decade for a car that will likely break down before the loan is paid off.

3. Payday Loans

These are predatory loans with effective annual interest rates that can exceed 400%. They are designed to trap desperate people in a cycle of poverty. This is not leverage; this is financial slavery.

4. “Buy Now, Pay Later” (BNPL)

Services like Afterpay or Klarna have popularized financing small consumer goods (clothes, shoes, makeup). While often “interest-free” if paid on time, they encourage overconsumption. Borrowing money to buy a pair of jeans is a mindset problem. It trains you to spend money you haven’t earned yet.

Part 3: The Hero (Good Debt)

Now, let’s look at how the rich operate.

The Definition

Good Debt is money borrowed to purchase an asset that appreciates in value, generates income (Cash Flow), or provides a significant increase in future earning potential.

Crucially, with Good Debt, someone else pays for it.

- Tenant pays your mortgage.

- Customer pays your business loan.

- Government subsidizes it via tax incentives.

The Characteristics of Good Debt

- Low Interest Rates: Usually secured by a hard asset (collateral), lowering the risk for the bank.

- Tax-Deductible: The interest you pay is often a write-off against your income.

- Income Producing: The asset puts money in your pocket every month.

- Inflation Hedge: The debt stays fixed while the asset value and income rise.

Examples of Good Debt

1. Investment Real Estate (Mortgages)

This is the holy grail of good debt. You borrow money to buy a rental property.

- You put 20% down. The bank puts 80% down.

- You collect rent.

- The rent covers the mortgage payment, the taxes, the insurance, and repairs.

- Whatever is left over is Positive Cash Flow.

The Magic: You own 100% of the asset, you get 100% of the appreciation, and you get 100% of the tax benefits, but you only used 20% of the money.

2. Small Business Loans

If you start a business and borrow $50,000 to buy equipment that allows you to produce $100,000 in profit, that debt is “Good Debt.” It has a positive Return on Investment (ROI). The equipment pays for the loan itself.

3. Education (With Caveats)

Student loans used to be good debt automatically. Today, it depends on the ROI.

- Good Debt: Borrowing $100,000 to become a specialized surgeon who earns $400,000/year. The math works.

- Bad Debt: Borrowing $100,000 to get a degree in a field where the average salary is $35,000. The math does not work.

Part 4: The Mathematics of Leverage (Why Debt Creates Wealth)

To truly understand why the wealthy love debt, we have to look at the math. This is called Cash-on-Cash Return.

Let’s compare two investors: Cautious Carl (Cash Buyer) and Leveraged Larry (Debt Buyer).

The Scenario

Both investors want to buy a rental property worth $200,000. The property appreciates (grows in value) at 5% per year. The property generates $15,000 per year in net rental income (after expenses).

Cautious Carl (The “Cash is King” Strategy)

Carl is scared of debt. He saves up and pays $200,000 cash for the house.

- Investment: $200,000

- Rental Income: $15,000

- Appreciation (5%): $10,000

- Total Return: $25,000

ROI=$200,000$25,000=12.5%

Carl made a respectable 12.5% return. He is happy.

Leveraged Larry (The “Good Debt” Strategy)

Larry understands leverage. He buys the same house, but he gets a mortgage. He puts 20% down ($40,000) and borrows the remaining $160,000. Because he has a mortgage, he has to pay interest (let’s say 6%). That costs him roughly $9,600/year in interest payments.

- Investment: $40,000 (Down payment)

- Rental Income: $15,000 (Gross) – $9,600 (Mortgage Interest) = $5,400 (Net Cash Flow)

- Appreciation (5%): $10,000 (Larry keeps all the appreciation, not just 20% of it).

- Total Return: $5,400 (Cash) + $10,000 (Value Increase) = $15,400

ROI=$40,000$15,400=38.5%

The Verdict

- Carl used $200,000 to make $25,000. (12.5%)

- Larry used $40,000 to make $15,400. (38.5%)

Larry’s money worked 3x harder than Carl’s money. Furthermore, because Larry only used $40,000, he could theoretically buy 5 houses with the same $200,000 that Carl used to buy one. If Larry buys 5 houses, he controls $1 Million in real estate. If the market goes up 5%, Larry makes $50,000 in appreciation. Carl only makes $10,000.

This is the power of Good Debt. It decouples your ability to build wealth from your personal cash limitations.

Part 5: The Tax Advantage (The Secret Weapon)

The benefits of Good Debt aren’t just about leverage; they are also about taxation. The tax code is written to incentivize investors and business owners.

1. Interest Deductibility

If you have a credit card (Bad Debt), you pay the interest with Post-Tax Dollars.

- You earn $100.

- The government takes $30 tax.

- You have $70 left.

- You pay the bank $20 interest.

If you have a business loan or rental mortgage (Good Debt), you pay the interest with Pre-Tax Dollars.

- You earn $100 revenue.

- You pay the bank $20 interest.

- You tell the IRS: “I only made $80.”

- The government taxes you on the $80, not the $100.

This effectively makes Good Debt “cheaper” than Bad Debt because the government subsidizes the cost.

2. Depreciation

When you own an income-producing asset purchased with debt (like a building), the IRS allows you to claim a “phantom expense” called Depreciation. You can tell the IRS the building is losing value (even if it’s actually gaining value in the real market) and deduct a portion of the building’s cost from your taxable income every year. This often results in Zero Tax Liability on the cash flow the property generates.

Part 6: Inflation Hedging (Paying Back with Cheaper Dollars)

In our previous article about Inflation, we learned that cash loses value over time. When you are a Saver, inflation is your enemy. When you are a Debtor, inflation is your best friend.

Why? Because debt is fixed, but money is fluid.

Imagine you take out a $2,000/month mortgage in 2025. That $2,000 feels like a lot of money today. It represents perhaps 40 hours of work.

Fast forward 20 years to 2045. Inflation has driven up wages and the cost of goods. A loaf of bread is $10. The average salary has doubled. However, your mortgage payment is still $2,000.

In 2045 dollars, that $2,000 might only represent 10 hours of work. It feels like “pocket change.” You borrowed “expensive” 2025 dollars, and you are paying the bank back with “cheap” 2045 dollars. Effectively, inflation is paying off a portion of your debt for you.

This is why governments love debt—they can inflate their way out of it. You can do the same.

Part 7: The Grey Area (Proceed with Caution)

Not all debt fits perfectly into “Good” or “Bad.” There is a grey zone where the debt depends entirely on how you use it.

1. Home Equity Loans (HELOCs)

A HELOC allows you to borrow against the value of your home.

- Good Use: Taking a HELOC at 7% to renovate your kitchen, increasing the home’s value by $50,000. Or using the HELOC as a down payment for a rental property.

- Bad Use: Taking a HELOC to pay for a vacation to Disney World or to pay off credit cards without fixing your spending habits.

2. Debt Consolidation Loans

This is taking one big loan to pay off many small loans.

- The Trap: Many people consolidate their credit card debt into a lower interest loan, feel a sense of relief, and then run up the credit cards again. Now they have the consolidation loan AND new credit card debt. This is financial suicide.

3. Primary Residence Mortgage

Is your own home an asset or a liability? Robert Kiyosaki argues it is a liability because it takes money out of your pocket (mortgage, tax, insurance) and doesn’t pay you. However, compared to renting, a fixed-rate mortgage acts as a forced savings account and an inflation hedge.Verdict: It is “Neutral Debt.” It is better than renting in the long run, but it won’t make you rich like a rental property will.

Part 8: The Risks (The Sword Cuts Both Ways)

We have praised leverage, but we must respect it. Leverage magnifies gains, but it also magnifies losses.

If you buy a $100,000 house with $20,000 down (5x leverage):

- If the market drops 20%, the house is worth $80,000.

- You still owe the bank $80,000.

- You have lost 100% of your equity.

If you had paid cash, you would still have $80,000 of equity. Leverage wiped you out.

The Cash Flow Cushion

The biggest risk with debt is Cash Flow Crunch. If you lose your job or your tenant stops paying rent, you still have to pay the bank. If you can’t pay, the bank takes the asset (Foreclosure).

The Golden Rule of Leverage: Never borrow money if you cannot survive the worst-case scenario.

- Do not rely on the asset appreciating.

- Rely on the asset Cash Flowing.

- Always keep a “Capital Reserve” (Emergency Fund) specifically for your investments.

Part 9: Strategies to Shift from Bad to Good

Most people reading this probably have some mix of bad debt. Here is the roadmap to cleaning up your balance sheet so you can start using leverage correctly.

Step 1: Stop the Bleeding

You cannot invest your way out of bad debt. The stock market returns 8-10%. Credit cards charge 20-25%. The math is impossible. You must pause all aggressive investing until high-interest consumer debt is gone.

Step 2: The Avalanche vs. Snowball Method

- Avalanche: Pay minimums on everything, and throw all extra cash at the debt with the highest interest rate. This is mathematically superior.

- Snowball: Pay minimums on everything, and throw all extra cash at the smallest balance. When it’s paid off, move to the next smallest. This is psychologically superior because you get quick wins.

- Pick one and execute.

Step 3: Fix Your Credit Score

To use Good Debt, you need the bank to trust you. You need a high credit score (740+).

- Pay everything on time.

- Keep your “Credit Utilization” low (don’t max out cards).

- Don’t close old accounts (history matters).

A high credit score is your “VIP Pass” to cheap money. It determines whether the bank lends to you at 6% (profitable) or 9% (unprofitable).

Step 4: Buy Cash Flow First, Luxury Later

Once you are debt-free and have capital:

- Borrow money to buy an Asset (Rental Property/Business).

- Use the Cash Flow from that asset to make the payments on a Luxury (Car/Boat). This is how the wealthy buy toys. They never pay for liabilities with their labor; they pay for liabilities with their asset income.

Conclusion: Mastering the Tool

Fire is dangerous. It can burn your house down. But if you learn to control it, fire can cook your food, warm your home, and forge steel.

Debt is fire.

If you use it to buy clothes, cars, and vacations, it will burn your financial house down. This is Bad Debt. Avoid it like the plague.

If you use it to buy cash-flowing assets, tax advantages, and inflation hedges, it will forge your financial freedom. This is Good Debt.

The goal is not to be “debt-free” in the sense of having $0 liabilities. The goal is to be “Consumer Debt Free” while managing a portfolio of healthy, high-quality, income-producing debt that is paid for by others.

Your Action Plan:

- List all your debts.

- Label them “Good” (someone else pays/tax deductible) or “Bad” (you pay/high interest).

- Create a plan to ruthlessly eliminate the “Bad.”

- Begin educating yourself on real estate or business investing to prepare for the “Good.”

Stop fearing leverage. Start respecting it. And then, use it.