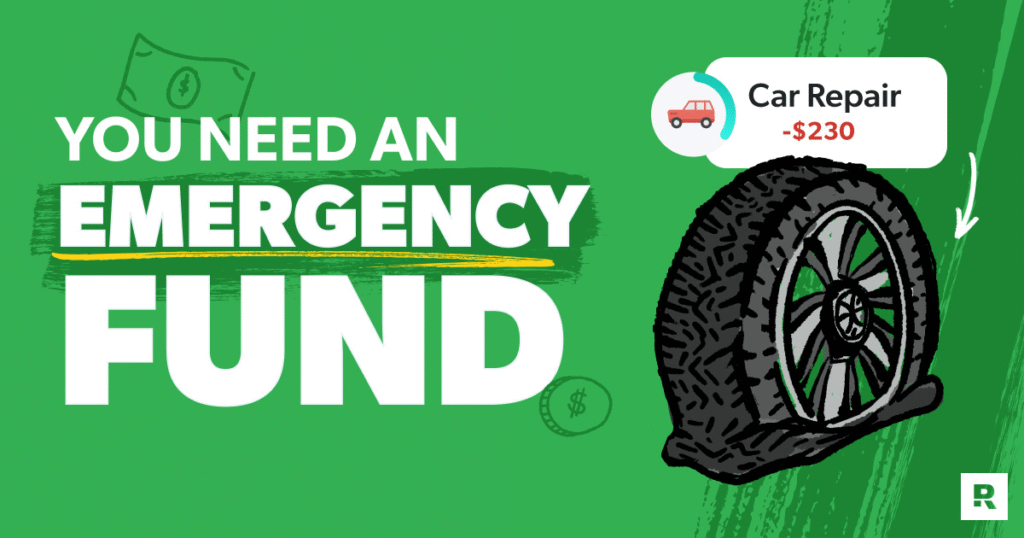

Picture this: It is Tuesday afternoon. You are sitting at your desk, sipping coffee, feeling like you finally have a handle on your monthly budget. Then, your phone buzzes.

It’s your mechanic. That strange noise your car started making this morning? It wasn’t nothing. It’s the transmission. The quote: $2,400.

For the average person, this phone call triggers immediate panic. It means swiping a credit card they can’t pay off. It means stress. It means the beginning of a spiral into high-interest debt that could take years to escape.

But for someone with a fully funded Emergency Fund, this phone call is just… an annoyance. It’s a transaction. You transfer the money, the car gets fixed, and life goes on without a financial crisis.

An emergency fund is the backbone of financial wellness. It is the buffer between you and the chaos of the real world. In this comprehensive guide, we are going to break down exactly how to build this safety net, where to keep it, and how to calculate the magic number that lets you sleep at night.

Part 1: What Exactly is an Emergency Fund?

An emergency fund is a stash of money set aside for the sole purpose of covering unexpected, urgent financial shocks.

It is not for a vacation. It is not for Christmas gifts. It is not for a down payment on a house.

It is self-insurance.

Think of it as a “Break In Case of Emergency” box. Its primary job isn’t to grow or earn high returns; its job is to be liquid (accessible) and safe (stable) when you need it most.

The “Starter” vs. The “Full” Fund

There are generally two stages to building this fund:

- The Starter Emergency Fund: This is usually $1,000 to $2,000 (or one month of expenses). You build this while you are paying off debt. It protects you from minor inconveniences (blown tires, broken appliances) so you don’t have to use a credit card.

- The Fully Funded Emergency Fund: This is built after you have paid off high-interest debt. This is the robust shield that covers major life events like job loss, medical emergencies, or divorce.

Part 2: The Psychology of Cash on Hand

Why is this fund so critical? The math says you should pay off debt first because credit card interest (25%+) is higher than savings interest (4-5%).

However, personal finance is 20% math and 80% behavior.

1. The “Murphy’s Law” Repellent

Murphy’s Law states: “Anything that can go wrong will go wrong.” It seems that trouble loves company. The moment you commit to getting your financial life in order, the furnace breaks. If you have no cash reserves, you are forced to borrow money to fix it. This reinforces the psychological belief that “I just can’t get ahead.” An emergency fund breaks this cycle.

2. The “F-You” Money

When you live paycheck to paycheck, you are trapped. You cannot quit a toxic job because you need the next check to pay rent. You cannot leave a bad living situation because you can’t afford a moving truck. An emergency fund gives you options. It gives you the power to say “No” to situations that no longer serve you.

3. Stress Reduction

Financial stress is a leading cause of divorce and health issues. Knowing you have $10,000 or $20,000 sitting in the bank lowers your baseline cortisol levels. You become a better employee, partner, and parent when you aren’t subconsciously worrying about the electricity bill.

Part 3: The Million Dollar Question: How Much Do You Need?

The standard advice is 3 to 6 months of expenses.

But that is a wide range. The difference between 3 months and 6 months could be $15,000. So, which number is right for you?

First, let’s clarify Expenses vs. Income. You do not need to replace your income; you need to cover your expenses. If you earn $5,000 a month but only spend $3,000 to survive, your calculation is based on the $3,000 figure.

The 3-Month Fund (Lean)

You can aim for the lower end (3 months) if:

- You are a dual-income household: If you lose your job, it is unlikely your partner will lose theirs on the exact same day. You still have cash flow.

- You have a stable career: You work in government, healthcare, or a tenure-track position with very low layoff risk.

- You rent: Your maximum liability for home repair is usually $0 (that’s the landlord’s problem).

- You have no dependents: It is just you (and maybe a cat).

The 6-Month Fund (Standard)

You should aim for the standard (6 months) if:

- You have children: Kids are expensive and unpredictable.

- You own a home: A new roof or HVAC system can cost $10,000 instantly.

- You are a single-income household: If the breadwinner loses their job, income hits zero.

The 12-Month Fund (Robust)

You should aim for the higher end (9-12 months) if:

- You are self-employed or Freelance: Your income fluctuates, and you don’t get severance packages or unemployment benefits.

- You work in a volatile industry: Tech startups, commission-based sales, or seasonal work.

- You have a high anxiety tolerance: If having a massive pile of cash makes you sleep better, the “opportunity cost” of not investing that money is worth the peace of mind.

How to Calculate Your “Bare Bones” Number

To find your number, strip your budget down to the survival level.

- Housing (Rent/Mortgage + Utilities)

- Food (Groceries only, no restaurants)

- Insurance (Health, Car, Life)

- Minimum Debt Payments

- Transportation (Gas/Bus fare to get to interviews)

Example: If your Bare Bones expenses are $3,000/month:

- 3 Months: $9,000

- 6 Months: $18,000

Part 4: Where Should You Keep It?

This is where many people get it wrong. They either keep it in their checking account (where they accidentally spend it) or they invest it in the stock market (where it might crash right when they need it).

Your emergency fund needs three traits: Liquidity, Stability, and Separation.

1. High-Yield Savings Account (HYSA)

This is the gold standard.

- Why: Traditional banks pay 0.01% interest. Online HYSAs (like Ally, Marcus, Capital One, SoFi) pay 4.00% to 5.00% (as of 2024/2025 rates).

- Liquidity: You can transfer the money to your checking account in 1-3 business days.

- Separation: It is usually at a different bank than your daily checking account. You don’t see the balance when you log in to buy groceries. Out of sight, out of mind.

2. Money Market Accounts (MMA)

Similar to HYSAs but often come with debit cards or check-writing privileges. This offers higher liquidity but slightly higher temptation to spend.

3. What to AVOID

- Physical Cash: Having $20,000 under your mattress is a risk for fire or theft. Plus, it loses value to inflation.

- Stocks/Crypto: Imagine you had your emergency fund in the stock market in 2008 or 2020. The market crashed by 30%. If you lost your job during that crash, your $10,000 emergency fund would have only been worth $7,000 when you cashed it out. Never invest your emergency fund.

- CDs (Certificates of Deposit): While safe, your money is locked up for months or years. If you need the cash today, you pay a penalty to access it.

Part 5: What Actually Counts as an Emergency?

Once you have the money, you must protect it. You need a strict definition of “Emergency.”

The Three-Question Test: Before touching the fund, ask yourself these three questions. If the answer is “No” to any of them, do not touch the money.

- Is it unexpected? (Christmas is not unexpected; it happens every December. Car registration is not unexpected. These should be budget items, not emergencies).

- Is it necessary? (A functioning car is necessary. A functioning air conditioner in Florida is necessary. A last-minute flight to a friend’s bachelor party is not necessary).

- Is it urgent? (Does this need to be paid today to prevent disaster? Or can I cash flow this by cutting back on spending for two weeks?)

Valid Emergencies:

- Job loss.

- Medical/Dental emergency.

- Emergency vet bill.

- Car breakdown (that prevents you from getting to work).

- Home repair (leaking roof, broken furnace, flooded basement).

- Unexpected travel for a family funeral.

Part 6: How to Build It Fast

Saving $15,000 sounds daunting. It can feel like climbing Everest. Here is how to accelerate the process.

1. The “Garage Sale” Weekend

Look around your house. The average household has thousands of dollars worth of unused items. Sell old electronics, clothes, and furniture on eBay, Poshmark, or Facebook Marketplace. Dump 100% of the proceeds into the fund.

2. Temporary Austerity (The “Fiscal Fast”)

Commit to a “No-Spend Month.” Cut all subscriptions, stop eating out, and buy only generic groceries. Challenge yourself to live on the absolute minimum for 30 days and shovel the savings into the fund. It is easier to suffer for a month than to suffer for a year.

3. Redirect Windfalls

Did you get a tax refund? A work bonus? A birthday check from grandma? Do not look at that money as “fun money.” Look at it as “freedom bricks.” Build your wall of security.

4. Pause Investing (Controversial but Effective)

If you have zero emergency fund, you are in a danger zone. It is mathematically acceptable to temporarily pause your extra 401k contributions (keep the match) or Roth IRA contributions for a few months to free up cash flow to build your safety net. Once the fund is full, turn the investments back on.

Part 7: Managing the Fund Over Time

Replenishing

If you have to use the fund, don’t feel guilty. That is what it is there for! You didn’t fail; the system worked. However, as soon as the dust settles, your number one financial priority becomes refilling the fund. Stop extra investing and discretionary spending until the bucket is full again.

Inflation Adjustments

Life gets more expensive. $10,000 in 2020 bought a lot more than $10,000 in 2025. Once a year, review your “Bare Bones” expenses. If your rent or insurance went up, you need to add money to your emergency fund to maintain that 3-6 month coverage.

Dealing with “Too Much” Cash

Is there such thing as too big of an emergency fund? Yes. If you have 2 years of expenses sitting in a savings account, you are losing money to inflation. That “lazy equity” should be working for you in the market. Cap your fund at a reasonable level (e.g., 6-9 months) and invest everything else.

Conclusion

Building an emergency fund is rarely exciting. It doesn’t give you the dopamine hit of buying a new car or seeing a stock double in value. It is boring.

But boring is good. Boring is safe.

When you have a fully funded emergency fund, you walk through life differently. You negotiate your salary with more confidence. You sleep deeper. You are harder to intimidate and harder to stress out.

The best time to start was five years ago. The second best time is today. Open a High-Yield Savings Account, nickname it “Freedom Fund,” and transfer your first $50. You are on your way.